Issue 3: Utilizing Standby Letters of Credit for Raising Capital, Business Credit and more

Issue 3: Utilizing Standby Letters of Credit for Raising Capital, Business Credit and more

Financing techniques no one will teach you.

Let’s get right into it. Continuing from the last issue, we’ll be sharing information about Standby Letters of Credit (SBLC) that can be obtained through the 🤡 banking system by most top international 🤡 banks.

We are fairly confident most of the information that will be shared in this issue is not known to the general public, will be unconventional, may look to be a scammy get rich quick scheme, impossible and could very well 🤯. We know. We’ll let you decide for yourself. However, this is all based completely on experiences of a anonymous cartoon and their partners by working within the confines of the 🤡 banking system to raise capital, helping clients make more money and fund projects globally.

This issue and the next will be longer than others as there is a lot of info and technicalities to cover. Hopefully you’ve got some free time to read a long-form article. We will do try to do our best to share the information in the simplest way possible such that the all Degens who may not work in finance or have a deep understanding of finance and the 🤡 banking system are able to understand.

Disclaimer: Information shared is by an anonymous cartoon for your own knowledge, potential usage and reading entertainment. Not financial, tax or legal advice. DYOR and discard if not useful.

Let’s start off by saying if you had shared with us the information below before we actually had to go through the hard route of learning it all, our initial reaction would be you’re a professional scam artist and everyone else whom you work with is the same. In order to prevent that, we feel we need to provide some context.

Many lawyers and 🤡 banking “executives” have informed us that we are TEACHING THEM about legal and banking! One of these 🤡’s once told us the information shared below (as they don’t know shit…NGMI) are nice “concepts and theory”…we proceeded to smile and nod. Lol.

In our world, most people have no clue what is fractional banking, have zero idea about the credit market and credit swaps. We don’t blame them. Access to information and having reference points is what’s required. So here we are looking to equalize information flow so that all of you smart people can rise. As the visionary behind our movement @BowTiedBull, often says Equal Opportunity, Unequal Results. Our intention for you anons is to use this information, copy it and use it for yourself if you like. Or not. You decide for yourself. Discard if not useful.

If all you know is retail banking, which we refer to as your typical personal/consumer banking, what you’re about to read will be extremely unconventional and odd. We recommend you please read about credit swaps and about the credit market (primary and secondary) so you can learn how you will be able leverage the usage of new or existing banking instruments to create credit for yourself to make investments on things you would like.

Context:

Access to Capital.

Our belief is no matter what you would like to do in this world, you will need access to capital. Those who can raise and get access to the most amount of capital can have a higher potential chance of winning.

E.g. 1: Think of this way. Let’s say Amazon and your business is competing. Do you think you can compete? Maybe you can or maybe you can’t. Amazon and similar corporates will LOSE money for 10 years and dry you out before you have a remote shot at making an empire as big as theirs. They don’t care. Yes, they’re ruthless. Now, think for a second. How do you think they can do that? Answer is simple. Access to capital. Even though, they don’t NEED the capital, they recently raised $18.5 Billion from a bond raise through the debt markets. That’s $18,500,000,000 US Tokens. Why? For the reason as stated before.

E.g. 2: You want to save the world by bringing free healthcare in developing and third-world countries and have the capacity/resources to bring together top-class doctors and nurses to treat patients….guess what? You NEED access to capital so you can pay for the services, build medical facilities and hospitals.

E.g. 3: You have children or have a family whom you want to provide for and you’d like to have them to start their life or career at a different starting point them most others….guess what? You NEED access to capital.

If you don’t care about saving the world or helping your family/loved ones and currently just have a regular day-to-day job (hopefully not for long!) and you’re looking to get income so you can survive while aiming to have financial freedom….guess what? You NEED to learn how to get access to capital such that you’re able to make investments in things you care about.

No matter what you want to do in the world. Things cost money. So. You NEED access to capital. Rant end.

1971.

Richard Nixon, President of USA at the time did one significant change to the planet. You no longer could go to the bank and exchange US Token for gold.

The impact? Central banks can push a button and make the money printer go BRRRR. Essentially, causing money to be printed from thin air.

Debt is greater than Income

Places like the US government, you’ll find the amount of debt/deficit that they have is FAR higher than the amount of income they are generating.

Growth = Function of Credit Creation

We live in a world of credit. If you want growth, you will highly likely need credit. Whether we like it or not, it’s the fact of the world currently….Till things change for the better hopefully.

E.g. Let’s say your business and our business both make the best pasta in the world. Both of our businesses use similar processes, employees, facilities etc. However, we understand credit and how to create credit while you may not. We have a clear competitive advantage. Why?

We can create credit -> get access to capital by leveraging the credit -> use that capital for investments and cashflow creation -> reinvest in our pasta business. We do that over and over again. Doing so, we will be able to have a quantum leap compared to you and both of our competitors because we have the capability and resources to do so.

Here’s a list of the top 50 🤡 banks in the world based on total assets from a simple Google search.

The above image highlights the Top 50 🤡 banks in the world as of 2020. Many of you may be banking with them for your day-to-day personal and business banking needs. Love ‘em or hate ‘em (we know most of us anon’s do hate them…including us for reasons to be shared later), everything below is unfortunately….with the usage of 🤡 banks. Till a time (not very far hopefully) that blockchain and crypto can solve it!

Standby Letters of Credit (SBLC’s)

Copied from the last issue. SBLC is defined as:

A guarantee that is made by the 🤡 banks on behalf of a client, which ensures payment will be made even if their client cannot fulfill the payment. SBLC’s are created as a sign of good faith in business transactions and are proof of a buyer's credit quality and repayment abilities and shows a company’s credit quality and ability to repay loans. Issued by a 🤡 bank on behalf of a client that is used as “payment of last resort” should the client fail to fulfill a contractual commitment with a third party.

In addition, they are used in situations in business where two parties (often in two different legal jurisdictions/countries) have an issue of trust and payment as to not having done business together in the past.

By its own nature and definition, only 🤡 banks can legally issue an SBLC (Standby Letters of Credit) or BG (🤡 Bank Guarantee). This is not only common sense, but actually regulated by 🤡 banking laws in most countries since these are debt obligations issued by bank. SBLC/BG must be UCP-600 (International Chamber of Commerce (ICC) rules) compliant and hence it must be issued by a licensed bank alone. Otherwise, it will not be compliant, regardless of the wording of the document. No 🤡 bank will ever accept it as collateral or even as a documentary credit if it’s not compliant.

The above is what SBLC’s typically were invented to be used for. Nowadays, there are many creative financing techniques which we’ll be sharing with you in this issue that they can be utilized to fund projects, businesses, get access to credit and for wealth accumulation purposes.

SBLC’s are primarily very popular in the commodities industry. This is because of the comfort it provides sellers that they would receive payment.

SBLC’s are generally backed by some sort of assets (real estate, equipment, art, stocks etc.) or simply liquid cash (in US/EUR/Any currency Token terms). In the SBLC’s world, we refer to it as cash-backed SBLC OR asset-backed SBLC. Typically, most are cash-backed.

Providers of SBLC’s or BG’s are a part of the “Secondary Market” or “Secondary Debt Market” transactions. They can be HNW corporations or individuals who hold bank accounts at the issuing 🤡 bank that contain significant amount of cash or assets. The Provider would instruct it’s issuing 🤡 bank to secure and encumber (i.e. freeze) cash in his own account and authorizes the bank to “cut” (an industry term meaning to create a financial instrument such as SBLC/BG; often called “cutting paper” or “commercial paper”). Effectively, the SBLC/BG is “leased” (how you lease a car) or “sold” (full purchase) to the Beneficiary (you or your clients) as a form of investment since the Provider receives a return on his commitment.

If you have the sufficient cash right now, you can pick up the phone and communicate with the 🤡 banks trade specialist or trade department to purchase an SBLC. To be frank, most of them don’t know shit as it’s not conventional for the purposes we’ll describe here.

Your second best and most likely used option will be to have a consultant, broker, or equity firm with sufficient knowledge, expertise, relationships and track record help you obtain a SBLC or any financial instrument. You could probably Google search to find companies or find people on LinkedIn who may have the expertise in this area. Our recommendation is to just make sure to ask the right questions to filter out scammers versus guys who know what they’re doing. These companies and/or individuals may charge you upfront costs for their time so be ready for that. If their costs happen to be outrageous, NEXT them. We consider $10K to $50K US Tokens as reasonable for their time and efforts. They will also have back end profits/percentage of the SBLC.

We don’t like this system as much as you do where you must “know people” and have “connections/contacts”. It’s what we’re working with. However, the information here should help you out quite a bit.

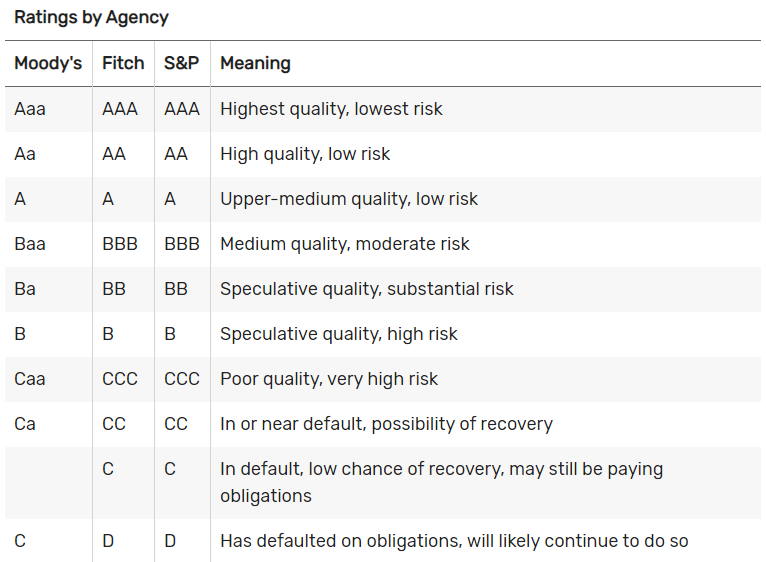

The best 🤡 banks to obtain an SBLC will be ones with expertise in international trade. Most European and some US 🤡 banks have this capability. Chinese 🤡 banks are great but you’ll have a very hard time from a monetization standpoint. Typically, based on the credit rating of the 🤡 bank which an estimate of how likely a 🤡 bank is to default or go out of business would determine how “good” an instrument is. The instruments also have ratings. AAA, AA, A rated instruments will be the easiest to work with for monetization purposes (explained later on in the issue). Non-rated instruments also exist in this instruments marketplace.

Top 🤡 Banks for instruments (our opinion):

🤡 HSBC UK

🤡 Barclays UK

🤡 Standard Chartered

🤡 UBS and DBS Singapore

🤡 UOB

🤡 Deutsche Bank

🤡 Most medium to large sized Swiss Banks

🤡 Bank Instrument Particulars (What You Must Know):

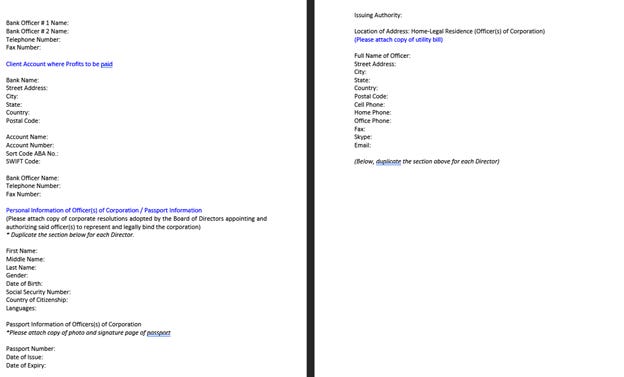

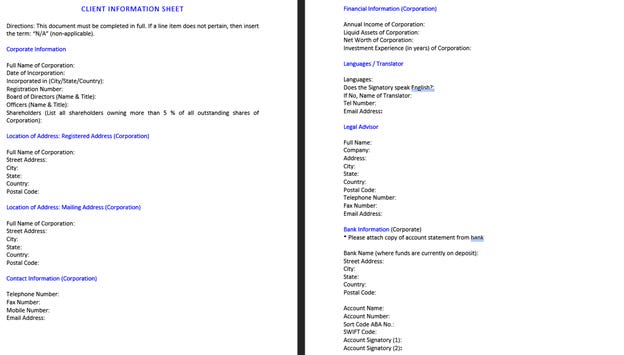

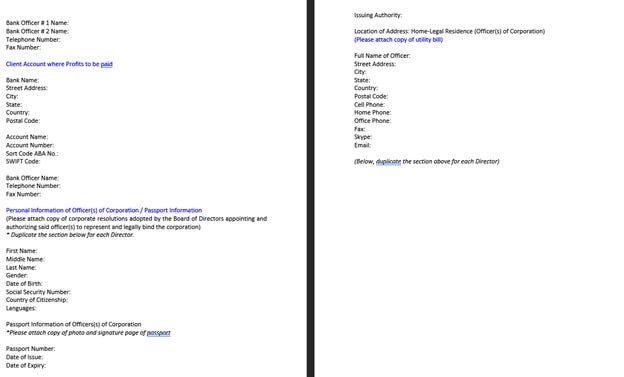

Proof of Funds (POF) = Attestation letter from your attorney showcasing you have the funds ready to do the transaction. Other options can include a redacted bank account statement or a 🤡 Bank Comfort Letter (BCL) showcasing the funds you have available for the underlying transaction.

CIS = Client Information Sheet. Similar to KYC (Know Your Client). Typically submitted before any transaction starts. Any info you provide here will be used to run compliance on you (if applying as individual), your corporation and as well as to do a authentic background check (since you’re providing your passport). This would be performed by attorneys, bank officers and/or ex three-letter agency individuals.

CIS Sample Instrument Type = SBLC, BG, MTN

Issuing Bank = 🤡 Bank issuing the instrument.

Face Value of the instrument = This is the monetary value in US/EUR Tokens term (or any other currency) of the SBLC or 🤡 bank instrument. E.g. Face value of $100MM SBLC is $100MM.

Sample Face Values: $1MM, $5MM, $8MM, $10MM, $50MM, $100MM, $200MM, $300MM, $500MM, $1BB and higher. We’ve seen a contract up to $2BB. Typically, they can go up to $50BB or higher.

Price = Cost of getting an instrument. Typical price ranges as follows:

Fresh cut (newly created) and purchased instrument - 72% of the face value

Seasoned (existing) and purchased instrument - 42% of the face value

Callable SBLC - 52% to 57% of the face value

Noncallable SBLC - 30% to 38% of the face value

Leased SBLC - 6% to 13% of the face value

The above prices can differ subject to varying factors such as:

Connections you have. Yes, we aren’t a fan of this as well.

If you or the party you’re going through has an “in” with the 🤡 banker at the instrument issuing 🤡 bank. The 🤡 banker’s benefit? They get back end profit (%) or “issuing fees”. Lol.

You or the party you’re going through is able to get special discounts due to bulk # of clients they bring in.

Many more other potential reasons.

E.g. 1: We knew of someone who allegedly could get clients a purchased new fresh-cut instrument in the teens range from a Top 50 🤡 bank.

E.g. 2: You want a leased $100MM US Tokens cash-backed SBLC. This will cost you in the range of $6MM to $13MM US Tokens depending on the issuing 🤡 bank and individuals you go through for the transaction.

By reading the above, this emoji may describe how you feel -> 🤯. Essentially, you are taking $6MM (for example) US Tokens and are turning it into approximately $60MM-$80MM US Tokens by leasing a bank instrument. You didn’t do real “work”, “create”, or “sell” anything to get to $80MM. However, you creatively used your (or other people’s) existing funds and/or credit line facilities to get access to more capital for your own benefit. You can kill your competitors by taking away all their sweet business. They are going to be caught slipping if you use what is shared here to your advantage! Our mind was certainly blown when we learned about the above.

Invoice Price = This is how you’ll often see an instrument quoted when you’re asking around for prices. Guys in this field will tell you the price is for example 40+2 or 6+2. The “+2” or “+(x)” is the percentage of the face value that would go to a consultant/broker/intermediary that helps you in the whole transaction to acquire the instrument and monetize it.

E.g. You’re the intermediary who is helping a client obtain a cash backed $100MM US Token 🤡 HSBC SBLC at a price of 40+2. Upon the success of this transaction (i.e. when the instrument is monetized…more on this coming up), you would get $2MM as your fees. These fees could be split with others if you’re working with other brokers and various parties. You may notice this is potentially a great way to make a substantial amount money as a consultant or broker. However, it’s not very easy. Just be careful of long broker chains as it would decrease the amount of US Tokens you make on the transaction.

Currency = This is the currency of the instrument. Pretty self explanatory.

Terms = 1 year and 1 day. Doesn’t matter if it is purchased or leased.

Expiry Date = Self explanatory.

Rolls and extensions = This is the number of years that the SBLC or 🤡 bank instrument contract can be extended for. It will typically be in the range of 2 to 5 years.

Example, you are purchasing a cash backed $50MM US Tokens SBLC. It would officially be due in 1 year and 1 day. However, because you are so smart by reading this guide, you knew that the language of 🤡 banking instruments is extremely vital. When purchasing or leasing the instrument, you made sure the language of the contract said “(X) Million or Billion with rolls and extensions”. When the one year is up, you can go to the bank and extend the SBLC for one more year.

Interest Rate = Can be Zero Coupon (0% interest) or anywhere up to 8% per year depending on varying factors.

Tranche = The tranches that the funds or instruments would be transferred to your monetization 🤡 bank. Tranches typically occur for large contracts.

E.g. Your contract amount is for $5BB with rolls and extensions. You will never have an issuing bank send a bank instrument for the full contract amount for such a large sum of money. As a result, it would be tranched in specific amounts. For this example, it would be likely $500MM tranches.

As an additional point, we will mention these instruments are issued and are up for grabs at all major Top 🤡 banks every single day without fail. It just matters if the individuals you’re dealing with are savvy and are able to get you what you need.

Process:

In simple terms: SBLC’s are supplied by the Issuing 🤡 Bank of the Provider to the Beneficiary’s (your or your clients) bank account at the Receiving 🤡 Bank and is transmitted inter-bank via the appropriate SWIFT platform alone (MT-760).

The Provider and the Beneficiary agree to enter into a Collateral Transfer Agreement (CTA) which governs the issuance of the SBLC/BG. The SBLC’s are specifically issued to the Beneficiary for a defined purpose and each contract would be customized. The underlying agreement (CTA) would have no effect on the wording or creation of the SBLC. This allows the Beneficiary (you or your clients) to use the SBLC to raise credit, to guarantee credit lines and loans or to enter trade positions or buy/sell contracts. This is key to this whole thing.

Step-by-Step Process:

Step 1: The Buyer (you or your clients) must have sufficient funds available in the form of liquid cash in a bank account or have active credit line facilities in a Top 50 🤡 bank (preferable 🤡 banks located in UK, Western EU, US, Canada, Singapore and Hong Kong). This showcases you have the financial wherewithal to purchase or lease the instrument.

Step 2: Buyer submits compliance documents. CIS Package and POF in the form of a 🤡 Bank Comfort Letter (BCL) or Redacted account statement. If utilizing a BCL, the language that your bank would need to provide is as follows:

“We [🤡 Bank Name] Bank confirm with full 🤡 bank responsibility that our client [Corporation/Individual Name] is in good standing with the 🤡 bank and there is a minimum of [X] Million of USD/EUR in the Buyer’s account free and clear of non-criminal origins OR that the Buyer’s credit facility is a) in good standing b) fully collaterized and c) the Buyer has access to a minimum of [X] Million of USD/EUR.”

Step 3: Issuing 🤡 Bank (Provider/Titleholder) will run compliance on the information package submitted and verify your funds are legit by confirming the bank officer’s IP address, 🤡 bank to bank email verification or 🤡 bank to bank phone call.

Step 4: The Provider/Titleholder will contact the Buyer and immediately issue a contract and delivery of the SBLC using the bank’s SWIFT system.

Step 5: Provider/Titleholder purchases the SBLC to be available for delivery within 24-48 hours.

Note: SBLC’s purchased by the Titleholder will be Titled in the Buyer’s name or Beneficiary’s name based on the instructions you or your client provide as the Buyer. Buyer doesn’t sign a contract till the SBLC is purchased.

Step 6: Provider/Titleholder confirms with the Buyer that the SBLC is available for purchase and is ready for delivery. Additionally, will be providing a contract for the Buyer to sign.

IMPORTANT: The below steps will apply if the Buyer and Provider are performing the transaction out of two separate banks. Everything can be done internally (and much easily) typically if the Buyer has funds in Barclays UK, HSBC UK, Credit Suisse ZH, or DBS Singapore (our opinion).

Step 7: Buyer’s 🤡 bank sends a MT-799 SWIFT message requesting a confirmation to the Titleholder/Provider’s 🤡 bank requesting an MT-799 RWA confirming the SBLC’s are in custody at the Provider’s 🤡 bank and available for purchase/delivery. Typically, a phone call or email to the Provider can be requested. Note: All communication is with a senior 🤡 banker from the Titleholder’s side and comes with full 🤡 bank responsibility.

Step 8: Provider/Titleholder’s bank replies with a MT-799 SWIFT confirmation with full 🤡 bank responsibility that the SBLC’s have been purchased and are in custody at the Provider’s bank ready to be delivered. Upon the SWIFT MT-103 SWIFT payment, the SBLC’s will be delivered immediately via MT-760 SWIFT into the Buyer’s account.

Note: The Buyer won’t be sending any payments until a confirmation from their own 🤡 bank officer is received that they’ve confirmed bank-to-bank with full banking responsibility that Provider will deliver the SBLC as stated in MT-799 confirmation.

Yeah.…This shit is extremely complicated. We know. To make the above extremely simple. Here’s the simplified version:

Step 1: You has money to do transaction.

Step 2: You submit documents about yourself or your company along with proof of funds.

Step 3: The 🤡 bank providing you the instrument will do legal, compliance and background check on you along with confirming your moolah is legit.

Step 4: The 🤡 bank providing you the instrument would give you a contract.

Step 5: The 🤡 bank providing you the instrument buys the instrument with you being the owner of that paper.

Step 6: They confirm they got the paper and is ready to deliver at your command. You also sign a contract to make sure everything so your ass is covered.

Step 7: Your 🤡 bank asks them to confirm by showing a POF of your SBLC/paper that it’s available to be bought and delivered to your 🤡 bank.

Step 8: The 🤡 bank giving you the instrument confirms with your own bank by internal 🤡 bank to bank messaging (SWIFT) system that they got your paper and can deliver it anytime. You pay, they deliver.

Note: SBLC sometimes is called “paper” because that’s exactly what it is. A piece of paper with (X) monetary value.

Be aware of the following:

Verbiage of the instrument - This is the language used on the instrument. Specific wording would have specific outcomes. This verbiage is what is utilized when banks send the instrument via the SWIFT messaging system. The typical wording or applicable rules would be as follows:

Irrevocable, Unconditional, Transferable, Divisible, Assignable

Sample Verbiage (Google) Time - You would very likely be heavily involved in the whole process above. Such as communicating with bankers, providing/approving verbiage of the instrument, letter of direction of where the funds are to be sent etc.

For things out of your control you may also face delays in various forms such as banker’s out of commission, verbiage, acceptance and confirmation of SWIFT messages. The timeframe for the whole process of issuing and monetizing SBLC’s can range from 10 international banking days to 45 international banking days. If delays occur, add 2-4 more weeks. We’ve never seen a transaction pan out in 10 international banking days. Our opinion is to always add 2 weeks to any timeframe that is quoted. Lot of the transaction is dependent on the issuing bank and receiving bank (talking and confirming SWIFT messages) along with the parties involved in helping you in the transaction. Crypto solves this. We wait till it’s full implementation occurs!

Monetization Process

Now. The fun part. Turning that paper into money! So you can blow it all on escor…we mean use it for business and investment purposes….We will never advise using the money for extracurricular activities.

Monetization is simply the process of converting an instrument into legal tender. i.e. liquid usable cash. Sometimes this process is also called “funding” the instrument.

Loan to Value (LTV) - This is the amount of the face value that can be monetized/funded. Here are some general guidelines based on the type of instrument you acquire:

Purchased = 70% to 90% of the face value.

Leased = 15% to 70% of the face value. This is subject to the rating of the instrument and issuing 🤡 bank.

E.g. You have a $100MM leased AAA rated 🤡 HSBC UK issued SBLC. If you were to monetize this said instrument, you can expect to get up to $75MM of liquid cash in your 🤡 bank account to be utilized for whatever you need.

E.g. 2: You have a $50MM leased non-rated 🤡 bank issued SBLC. Typically, you should expect to be on the lower end of the spectrum as it’s a non-rated 🤡 bank. This non-rating could be for example developing nations or third-world countries where their 🤡 banking system isn’t considered strong from an international standpoint.

In general, 🤡 banks will monetize only an “owned/purchased” instruments. The process would entail 🤡 banks receiving the instrument and drawing down a line of credit to provide you liquid cash.

🤡 Banks will not monetize a “leased” instrument. In contrast to a purchased or owned SBLC where the buyer is the official owner of the instrument and in turn would be able to lease the SBLC out to a Third Party, a “leased SBLC” cannot be “leased out” any further. Meaning if you own the instrument in your corporations name, you can “lease” it out on in the market effectively creating a strategy to earn interest.

If you are looking to monetize an SBLC, you will want to find a monetizer who can give you a decent LTV on the instrument. LTV’s are assessed by the strength of the security of the instrument and the banks credit worthiness (i.e. rating).

There are private monetizers who would monetize a “leased” instrument.

Although a leased instrument is not considered an “asset”, it can still be monetized by a resourceful Monetizer. Such resourceful Monetizers possess the capacity to a draw a line of credit against “leased” instruments and use part of the cash to pay the client “Non Recourse Monetization Payment” (often up to 70% of the value).

Non Recourse means it’s funds you don’t have to return/payback. Yes, you read that right. Technically, free money. How does this work? This occurs when the issuing 🤡 bank will send the instrument to the monetizer’s 🤡 bank with the monetizer being the beneficiary of that instrument (not you or your client). In turn, what the monetizer will do is keep the instrument, draw down their own line of credit and give you a non-recourse loan (i.e. loan you don’t pay back). The LTV for non-recourse loans is 30%-70% based on a variety of factors from the monetization party. What’ their benefit? They trade the shit out of the instrument to generate easy 2X-10X returns and make all that cash they gave you back and then some.

The Monetizer then takes the balance of the money from the Line of Credit and places these funds into Trade/PPP (coming up in next issue) using a proprietary trading platform.

Types of Monetizers: Private Companies, Family Offices, 🤡 Banks, Trading Platforms

EU regulated 🤡 banks for political reasons, will avoid as much as possible certain countries such as Latin American countries, China, Russia, Ukraine. If instruments being issued are from 🤡 banks in these countries, you will likely have to find a domestic monetization party or a party who will work with non-rated instruments. Expect a low LTV.

Notes:

Many resourceful monetizers are typically located in SG, EU, UK and US. With most of them being in the former countries.

As SBLC’s are not a very “popular” form for funding vehicle and most people are use to giving away the farm (in terms of equity in the business), you’ll find when you raise questions or provide your knowledge based on reading this issue, they will look at you very oddly as if you’re speaking an alien language.

Never bring an SBLC for monetization to a Canadian bank. They don’t know shit. You were warned.

Utility of the SBLC:

The great utility of the SBLC is that it can be used in practically any situation in which one party to a contract is concerned with the other party’s ability to perform.

Other widely use cases:

To ensure payment or performance in financing

Corporate transactions, M&A

Real estate transactions, leases on real and personal property

Fund Projects and businesses globally - Explained with examples in previous issue

Obtain credit - Lines of Credit for corporate against the SBLC

There are some 🤡 banks (you’ll have to find) that will take the issued SBLC and give you a line of credit against it for up to 90% of the face value. Thus, giving your business great leverage to to use capital for expansion and investment purposes. Most of these 🤡 banks are located in SG and EU.

Enter into Trade Programs and Buy-Sell Contracts - See next issue on PPP.

We seem to be running out of space due to the email length limit. Ending the issue here and will send the next one shortly after this one for continuation.

We hope you now know more about high-level finance and creative techniques than most of your peers and competition by reading this issue.

As always, DYOR, fact check and discard if not useful. This is just an anonymous cartoon on the internet.

Subscribe and share if you liked what you read!

This is insane.

So if I get it right, let's say I have a new SaaS venture that gets $44MM in funding from VCs. I can then buy a seasoned SBLC for $100MM and use the bank's AAA credit to get $75MM and use that to fund development without giving up any more ownership.

If the venture goes bankrupt, that's a lot of money that went up in smoke. Or am I missing something?